The Death of the Middle

Why the world's greatest brands are being squeezed from both ends. Part one of two.

I wore Nike for twenty years. Then, a couple of years ago, I looked.

For two decades my feet ran on faith. Nike Zoom for the gym, Vomero for the long walks I take to think. I never compared, never shopped, never wondered. The swoosh had earned the right to my attention a long time ago. That is what a great brand buys: the end of the search.

Then, on a slow afternoon, I actually walked the wall of a running store and read the boxes. What I found was not a competitor to Nike. It was a continent. Equal cushioning, often better. More choice across more use cases. A spread of prices that Nike alone had never offered me. Shoes engineered for the precise thing I do, by companies I could not have named three years earlier. I left in Skechers for the everyday and Hoka for the walks. I have not gone back.

I am not telling you this because my shoe rotation matters. I am telling you because the moment I looked, the moat was already gone. And what happened on that shelf is happening to almost every great brand of the last century, all at once, for reasons that have nothing to do with shoes.

The story is not that global brands are dying. Apple is the most valuable brand on earth and more dominant than it has ever been. Hermès just became the most valuable luxury house in the world. The story is stranger and more useful than decline.

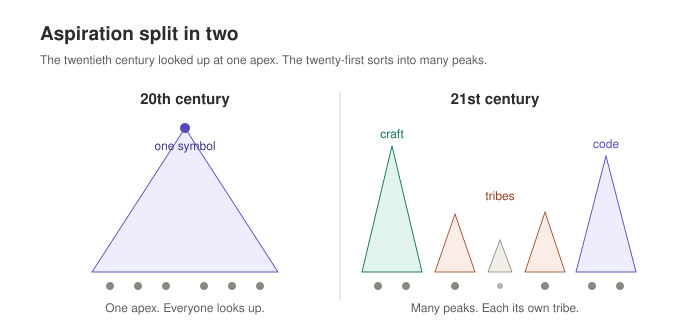

Aspiration did not die. It split in two.

The premium end is consolidating harder than ever. The accessible and tribal end is exploding. And the vast, comfortable middle, the place where most of the twentieth century’s great brands actually lived, is being squeezed out of existence from both sides.

This is the death of the middle. Let me show you how we got here.

When brands were larger than life

For most of the last hundred years, a brand was not a product. It was a promise you could not verify.

Think about what you were really doing when you bought a Rolex in 1985, or a bottle of Coca-Cola in a country whose language you did not speak, or a pair of Levi’s behind the Iron Curtain. You had no way to inspect the movement of the watch, no way to audit the syrup, no way to test the denim. You were buying trust, and the brand was the receipt. What you paid for when you bought a great brand was not the product. It was the right to stop checking.

That trust was expensive to build and even more expensive to fake, which is exactly why it was worth so much. It took decades of consistent quality, controlled distribution, and a single unwavering story.

Coca-Cola spent the better part of a century welding itself to American optimism until a red can could stand in for an entire idea of the good life. Rolex turned a precision instrument into a portable verdict on whether you had made it. The Ford Mustang sold steel and rubber, but what crossed the counter was the feeling of an open road and a younger version of yourself. Apple convinced two generations that the tool you compute with says something true about the kind of mind you have.

These were not marketing triumphs. They were cultural institutions. They worked because four things were scarce at once: the ability to manufacture at quality, the ability to design something beautiful, the ability to distribute it everywhere, and the patience to tell one story for thirty years. Whoever held all four held a fortress. The Beatles were a brand in exactly this sense. So was Marlboro, so was Sony, so was Mercedes. The whole world looked up at the same small set of symbols and wanted in.

The fortress depended on a quiet assumption that nobody questioned because nobody had to. The assumption was that those four scarcities would stay scarce.

They did not.

The great commoditization

Every wall of that fortress has been quietly torn down in the last twenty years, and most incumbents did not hear the demolition.

Manufacturing

Start with manufacturing. The contract factories of Vietnam, China, and Indonesia that make the world’s best sneakers do not work for one brand. They work for whoever sends a purchase order. The same supplier that perfects a midsole for a household name will perfect it for a startup that did not exist at the last Olympics. Quality, the thing that took Toyota forty years to systematize, is now something you can rent by the container.

Design

Design followed. The expertise that once lived inside a handful of studios in Portland and Milan now lives in software, in shared visual culture, in a global class of designers who trained on the same references and post to the same feeds. A small team today can produce work that looks every bit as considered as a heritage house. The aesthetic floor of the entire market has risen, which means aesthetics stopped being a differentiator and became table stakes.

Distribution

Then distribution collapsed in price. For most of history, getting a product in front of a billion people required a balance sheet that only a few hundred companies on earth possessed. Shelf space, television, global logistics: these were the real moat, more than the product ever was. Social platforms vaporized that cost. A brand born in a bedroom can now reach the same billion people for the price of a phone and an idea, and the idea travels for free if it is good enough.

Information/Trust

The last wall was the most important and the least discussed. Information went symmetric. The reason you paid for trust was that you could not check. Now you can. Before you buy anything, you can read a thousand strangers who already own it, watch it tested to destruction, compare its specifications against every rival in the category, and know within minutes whether the promise is real. The brand was the receipt for trust precisely because verification was impossible. Verification is now free, instant, and everywhere.

Put those four collapses together and you get the central fact of modern branding.

When everyone can make a good product, and everyone can find out, “good” stops being a moat.

What once took decades and a fortune now takes a few years and a funding round. The barriers to building a credible, beautiful, high-quality, globally available brand have fallen so far that credibility, beauty, quality, and reach have all become commodities.

This is the part where most analyses stop and declare the global brand dead. They are wrong, and the reason they are wrong is the most interesting thing in this essay.

Two doors: Code and Craft

If commoditization were the whole story, the strongest brands would be fading fastest, because they have the most premium to lose. The opposite is happening at the very top. So the real question is not whether commoditization is real. It is why some brands are immune to it and others are not.

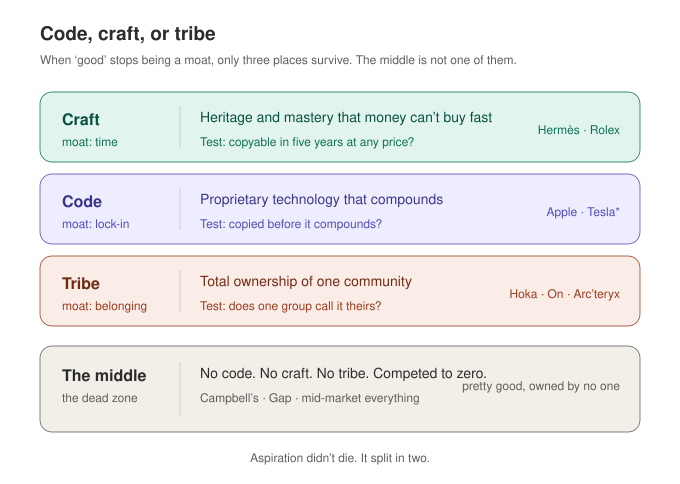

The answer is a single test.

A brand survives only if it owns something that cannot be copied.

Everything else gets competed to zero. And it turns out there are only two doors into that fortress. Call them Code and Craft.

Through the first door walk the brands whose advantage is proprietary, integrated, compounding technology. Apple is the purest case. It remains, by Interbrand’s count, the most valuable brand in the world, and it holds that position in a phone market where the hardware itself has long been commoditized. Anyone can buy the same OLED panels and the same camera sensors Apple uses. What they cannot buy is the silicon Apple designs, the operating system tuned to it, and above all the ecosystem that makes leaving feel like emigration. The moat is not the chip. The moat is the switching cost the chip made possible. That is Code: technology that compounds into lock-in.

Through the second door walk the brands whose advantage is irreproducible craft, scarcity, and heritage, accumulated over so long that money alone cannot buy a shortcut. Hermès has no technology moat whatsoever. It has something arguably stronger. In April 2025 its market capitalization passed LVMH’s to make it the most valuable luxury company on the planet, on roughly fifteen billion euros of revenue at an operating margin north of forty percent, the highest in the industry. You cannot disrupt a Birkin with a better supply chain. The waitlist is the product. The decades are the product.

That is Craft: scarcity and mastery that time alone can mint.

Here is the framework worth keeping. Footwear, packaged food, mass apparel, mid-market everything: these categories have access to neither door. Their technology is a purchasable input, not a proprietary system. Their heritage, however real, no longer commands a premium the buyer cannot verify away in an afternoon on the wall of a shoe store. They have no Code and no Craft. And a brand with neither door has only one place left to stand, which we will come to in a moment.

Watch what this framework predicts, because the predictions are uncomfortable.

It predicts that the middle dies even inside luxury. And it does. While Hermès climbed, LVMH’s 2024 revenue slipped about two percent to roughly eighty-five billion euros and net profit fell seventeen percent. The difference is not that one company is well run and the other badly. The difference is that Hermès sells pure scarcity and LVMH increasingly sells accessible luxury, the affordable handbag, the airport perfume, the entry-level aspiration. Accessible luxury is the middle wearing a designer label, and the middle is exactly what is under pressure. Even within the cathedral, the nave is emptying while the altar fills.

It predicts that the most American of brands, the ones built entirely on twentieth-century scale and narrative, would be the most exposed. And they are. In late 2024 Campbell, a company that had sold soup under its own name for a hundred and fifty-five years, voted to drop the word “Soup” from its name and become, simply, The Campbell’s Company. Read that again. The most iconic soup brand in the world decided that being known for soup was a liability, because soup has become a battlefield where store brands win on price and nobody wins on story. The strategy now is to run toward snacks, which is to say toward anything with a little more pricing power than a can of condensed tomato. That is not a rebrand. That is a refugee fleeing the middle.

And it predicts the most important thing of all about Code, which is that a technology moat is a clock, not a wall.

It holds only as long as the technology compounds faster than rivals can copy it. The moment it stops compounding, the brand falls back toward the middle like everyone else, and no amount of heritage can save it. We have a live experiment running right now, and its name is Tesla.

For years Tesla looked like permanent Code, a brand whose software, batteries, and charging network defended a premium position that should have been impossible in a commodity business like cars. Then the moat thinned. In 2025, BYD overtook Tesla as the world’s largest seller of battery-electric vehicles, delivering more than 2.2 million to Tesla’s roughly 1.64 million, and Tesla posted its second consecutive annual decline in deliveries. The moment its technological lead narrowed, Tesla was dragged into exactly the place its premium was supposed to protect it from: price wars and margin compression. Notice what Tesla is doing in response. It is racing toward robotaxis and artificial intelligence, which is to say it is trying to dig a new well of Code before the old one runs dry. Whether it succeeds is the most interesting question in the automotive world. That it must try at all proves the rule. Code is rented from the future, and the rent comes due.

So the map is clear. Three places are safe. The Code fortress. The Craft fortress. And one more, the place a brand goes when it has neither but refuses to die.

That place is the tribe.

The rise of the tribes

While the world wired itself together into one connected market, something contrary happened to the people inside it. They fragmented.

We assumed that global connection would produce global taste, that as everyone got online everyone would converge on the same few symbols. The reverse occurred. The more connected we became, the more finely we sorted ourselves: by geography, by income, by education, by politics, by aesthetic, by the specific niche of the specific hobby we have chosen to organize our identity around. Connection did not dissolve our tribes. It let us find them.

And our trust moved with us. The twentieth century trusted institutions, the brand, the network anchor, the national newspaper, the expert. The twenty-first century trusts the community, the group chat, the forum of obsessives who have tested every product in the category and owe no allegiance to anyone selling it.

Authenticity beat aspiration, because aspiration asks you to look up at a symbol and authenticity asks you to look around at your people.

A brand no longer needs to be admired by everyone. It needs to be trusted by someone specific.

This is the paradox the commoditization story misses. Production went global. Meaning went local. The factory that makes your shoe sits in a global supply chain that spans three continents, but the reason you chose that shoe is a small and particular story about a community you belong to, a use case you care about, a value you hold. The supply chain is universal. The belonging is not.

Which is why the brand that tries to mean something to everyone now ends up meaning nothing to anyone. A tribe will defend a brand that speaks precisely to it with a loyalty no mass brand can buy. But that same precision is invisible, even slightly embarrassing, to everyone outside the tribe. You cannot be a tribe and a monument at the same time. You have to choose.

No one shows the cost of failing to choose more clearly than the company I stopped buying.

Nike: the view from both ends

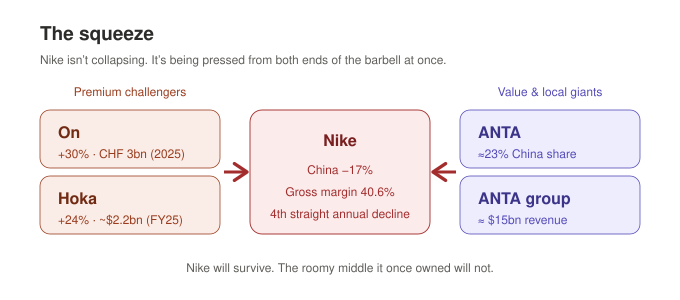

Nike is the most important case study in modern branding precisely because it is not collapsing. It is something more instructive than that. It is being squeezed from both ends at once, in real time, by forces it did not create and cannot fully control.

Remember what Nike was. It did not sell shoes. It sold the idea that you, too, could be great, and it rented the proof from the greatest humans alive. Michael Jordan made the swoosh mean transcendence. Tiger Woods made it mean dominance, Serena Williams made it mean unstoppable will. “Just Do It” was not a slogan. It was a global creed, three words that worked in every language because they pointed at something underneath language. For a generation, Nike was not a participant in the culture of achievement. Nike was the culture of achievement. That is as large as a brand has ever been.

Now read the recent numbers, and read them as structure, not scandal. In the quarter ending November 2025, Nike’s revenue was roughly flat at $12.4 billion, but gross margin fell three full points to 40.6 percent and net income dropped about a third. Greater China, long the engine, fell almost seventeen percent. Converse, its own subsidiary, fell thirty. The stock was heading for its fourth straight annual decline, and the company’s market value had fallen about a fifth from its peak of roughly $121 billion. The new chief executive, a Nike lifer brought back out of retirement to fix it, told investors the company was in the “middle innings of our comeback.” I would gently suggest the game is harder than an inning count implies, because Nike is losing at both ends of the field simultaneously.

At the premium end, the technology that justified Nike’s pricing has been commoditized. The cushioning science that once felt like magic is now available, often in a more specialized form, from companies that exist to serve one kind of runner extremely well. At the accessible and tribal end, a swarm of challengers has taken the use cases Nike was too big to love. And in the middle, where Nike actually lives, there is no longer anyone to sell to, because the middle is the thing that is disappearing.

Some of the wound is self-inflicted, and this is the part founders should study most closely. In its push to sell directly to consumers and capture the margin, Nike pulled back from the wholesale partners and the retail shelves that had been its distribution moat. It vacated space on the wall of the very store where I went looking. And the challengers walked straight into the gap, onto the shelf, into the hand of a customer who was, for the first time in twenty years, willing to look. You can see the correction underway: in that same recent quarter, Nike’s wholesale revenue rose eight percent while its own direct channel fell. The company is climbing back onto the shelf it abandoned. But the shelf is crowded now, and the customer has learned the most dangerous habit a great brand can teach: she has learned to compare.

This is not the death of Nike. Nike is enormous, brilliant, and entirely capable of finding a defensible position. It is the death of the kind of brand Nike was allowed to be: the universal symbol that did not have to choose a tribe because it was everyone’s tribe. That brand cannot exist in the market we now live in, and Nike’s struggle is simply the largest, most visible proof.

To see who took the ground, look at who walked out of the store on the customer’s feet.

The challengers

The challengers did not beat Nike at being Nike. They refused to play that game at all. Each one picked a door, or picked a tribe, and went deep where Nike was forced to stay wide.

On, the Swiss brand with the strange cloud-like soles, walked through the Craft door and built a premium runner’s brand from nothing. In 2025 it passed three billion Swiss francs in sales, up thirty percent, at gross margins around sixty percent that most apparel companies can only dream about. Its growth in Asia nearly doubled. It did not ask to be everyone’s shoe. It asked to be the discerning runner’s shoe, and charged accordingly. Hoka did something similar from the maximalist-cushioning direction. Inside Deckers it grew about twenty-four percent in the most recent fiscal year to roughly $2.2 billion, taking the exact customer I turned out to be: someone who walks a lot and wanted a shoe built for that and nothing else.

Then there is ANTA, which is a lesson in scale that most Western readers have not absorbed. The Chinese group’s 2024 revenue reached roughly seventy billion yuan, near ten billion dollars, and combined with Amer Sports, the portfolio it controls, the group cleared fifteen billion. In its home market it now holds around twenty-three percent share, ahead of Nike’s roughly twenty-one. It did not win China by being a better global brand. It won by being a better local one, investing in local athletes, local design, and a value-for-money proposition aimed squarely at a national identity Nike could never authentically claim. And through Amer Sports, ANTA owns Arc’teryx and Salomon, two brands that themselves walked through the Craft door into the most specific of tribes: the technical climber, the trail runner, the person for whom the gear is a statement of seriousness. A single Chinese conglomerate now spans from mass-market value to alpine prestige, owning multiple tribes at once while declining to compete for the empty middle.

The pattern repeats across the world. Salomon trail shoes have become an unlikely urban status symbol. Arc’teryx jackets signal a tribe long before they signal warmth. Lululemon turned yoga apparel into an identity. Vuori did it again, slightly downstream. Specialized brands across Asia, Europe, Latin America, and Africa are winning narrow categories in their own backyards that no global giant will ever bother to contest. None of them is trying to be the next Nike. Each is trying to be the only brand for one specific person doing one specific thing.

But I promised you both sides, and here is the side the challenger story usually hides. Owning a tribe is not a guarantee. It is a tightrope. A tribe that lifts you can also leave you the instant you betray it, and the most common betrayal is the one growth demands: trying to become bigger than your tribe. Allbirds is the cautionary monument. It rode a perfect tribe, the sustainability-minded coastal tech crowd, to a multi-billion-dollar public listing. Then it over-expanded into retail, diluted the thing that made it specific, and watched the tribe quietly leave. By the second quarter of 2025 its revenue had fallen more than twenty percent year over year to under forty million dollars, a fraction of its former self, the stock a ghost of its IPO. The tribe is a real moat, but it is a moat you can drain yourself, simply by deciding you would rather be a monument.

So the new normal is not loyalty to one dominant brand. It is the opposite. I now own Skechers and Hoka and probably should add a trail shoe, and I feel no disloyalty whatsoever, because I never swore an oath. Consumers did not become disloyal. They became plural. We wear three brands at once and belong to several tribes, and the brand that demands to be our only one has misunderstood the century it is selling into.

The Big Question

Step back and the shape is unmistakable. The middle is not a position. The middle was never a position. It was a moment, the lag between when a brand earned its lead and when the world caught up. For a hundred years that lag was long enough to build cathedrals inside. Now it is measured in quarters. The brands that survive will be those that own a door, Code or Craft, or own a tribe so completely that no global giant can be bothered to fight for it. Everyone else is competing for a space that is closing.

Which leaves the question I have been circling this whole essay, and it is a builder’s question, not a critic’s. If the moat is gone and the middle is dead, then what, exactly, do you build now?

Can a truly global brand still be born in a world this fragmented, or has the era of the universal symbol simply ended? Will the next great brands be ecosystems rather than icons, communities rather than logos, things you join rather than things you admire? What does artificial intelligence do to all of this, when it hands every founder on earth the same design, the same code, and the same reach, and accelerates the fragmentation into not thousands of brands but millions? And if trust has migrated from the institution to the network, does the future belong to brands at all, or to the creators and communities that brands will increasingly have to rent?

I have a point of view on each of these, and it is more optimistic than this diagnosis might suggest. The death of the middle is not the death of branding. It is the end of one way of being a brand and the difficult, thrilling beginning of another.

But that is the builder’s playbook, and it deserves its own essay.

The greatest brands of the twentieth century united billions of strangers around a single dream. The question for the twenty-first is whether greatness and universality can still share the same sentence, or whether the future belongs entirely to the brands that choose to be loved deeply by a few rather than admired faintly by everyone.

You tell me, what do you think?