The $65B GCC(Offshoring) Model Is Under Stress.

A CEO's Guide to What Breaks and What Comes Next

India’s Global Capability Center (GCC) model has been on an exponential trajectory. With over 1,800 GCCs employing approximately 2 million professionals across IT and IT-enabled services, the industry delivers over $64.6 billion in revenue, growing at nearly 14% annually. Most Fortune 500 companies from Microsoft, Amazon, Nvidia, Samsung, JPMC, National Australia Bank, Volvo and more have embraced and doubled down on the model. India commands over 45% of the global market share and continues to expand. Projections point to 2,400+ centers by 2030, generating $100 billion in revenue. Growth, capabilities, talent, innovation all seemingly unstoppable.

But I believe the GCC model stands at the edge of a cliff.

The critical question: does it take flight from here, or does it hurtle downhill?

Having built and managed GCCs of all sizes over two decades, I’ve witnessed firsthand the extraordinary value this model delivers. Yet it now faces forces that demand a fundamental rethink. The GCC industry was modeled on IT services, which today has begun to stall. I wrote about these impending headwinds in March 2025. Hiring in IT services, which typically exceeded 200,000 by this time of year, has been close to zero. To understand what lies ahead, we must first reflect on the road that led us here.

The GCC model’s success has rested on a powerful convergence of forces:

Currency arbitrage delivering 85–90% real estate savings and 4–5X labor cost efficiencies;

Demographics that supply ~2.1 million passionate, hardworking English-speaking, tech-skilled graduates annually and will persist through at least 2035;

Digital dexterity, proven across three decades of technological waves from ERP and Y2K to SaaS and now AI

Education and training ecosystem that augments engineering schools

Government incentives like Export processing zones and tax incentives

Technological advances in connectivity, cloud, and mobility that enabled seamless global collaboration.

Together, these created a massive tailwind, one that, despite repeated negative predictions, has only widened the gap.

But the model inherited from large IT services pioneers like Infosys, Wipro, TCS, HCL also carries structural weaknesses. And today, several ground shifts are beginning to undermine it in fundamental ways. Let’s examine them.

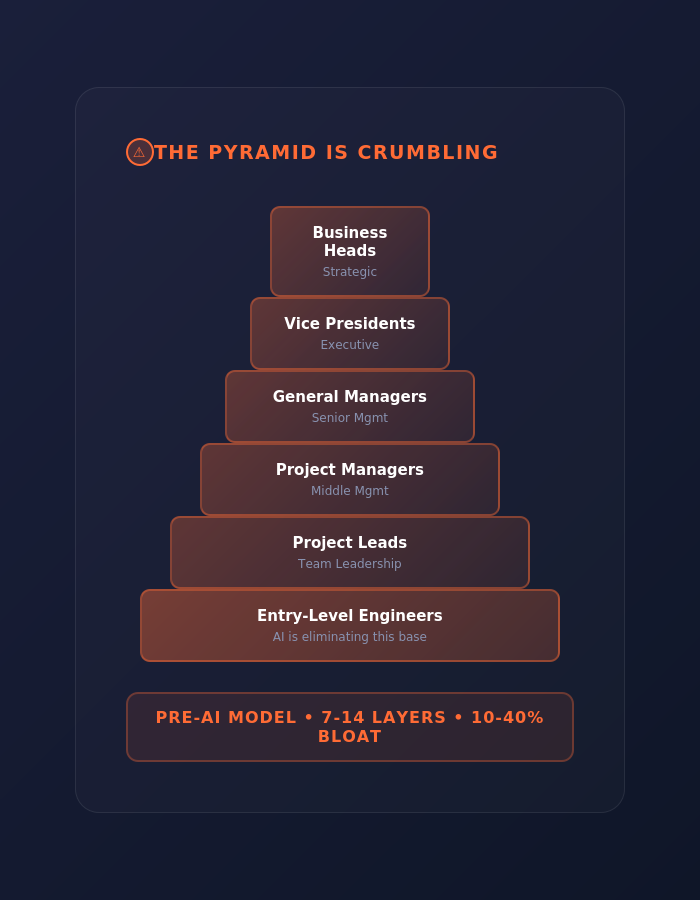

Defunct Organizational Model

GCCs largely replicated the “Pyramid” shaped organizational structure of IT services firms. Approach is to hire large numbers of young graduates, train them, deploy them to projects, and layer management to ensure oversight, delivery, and control. This worked because arbitrage was large, hours were long, and aspirational talent was willing to go the extra mile. Over time, layers were added to bridge time zones, create domain depth, and manage scale but the focus remained oversight-heavy.

Meanwhile, software development itself evolved. Agile, full-stack engineering, and Amazon’s “two-pizza teams” flattened organizations and reduced the need for managerial layers. Yet many GCCs today still operate with 7–14 layers between a frontline engineer and senior leadership, creating systemic bloat. I’ve personally seen GCCs with 10–40% excess headcount, hidden behind billion-dollar savings narratives.

When you’re delivering $1B in savings, no one questions a $100M - $200M inefficiency.

In an AI-first world, this structure is fragile and increasingly indefensible.

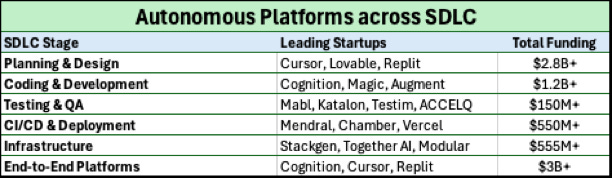

The AI Hammer

The pace at which AI evolves to deliver software code is rapidly diminishing the need for entry-level developers. In the previous era, armies of junior graduates maintained legacy software solving mostly repeatable problems requiring someone to identify and patch. Developers gradually moved to development projects and up the value chain. Today, faster, fully automated AI solutions or autonomous platforms are eliminating this need, moving toward self-remediation. Some examples below.

Organizations today are pyramid-shaped: large numbers of developers at the bottom, increasingly reduced layers of managers on top. If AI eliminates the base, we shift to a diamond-shaped organizational model.

The biggest challenge? For a diamond-shaped organization to succeed, all middle layers must be hands-on, high-impact developers, which isn’t the case today.

In a country with 8 million IT professionals, at least 30%+ occupy middle layers. How do we transition them to this new world?

Culturally in India, most developers don't want to remain developers after 4-5 years; they move to middle management and become people managers. Exceptions exist, but this is largely true. How do we reward, sustain, and keep talent excited about being developers for 20-30 years? This is the hardest problem; it's deep-rooted with a sense of success attached to it.

“AI Shoring”

There was an implicit barrier to becoming a software engineer, you needed an engineering degree or, as a non-engineer, spend years learning basics before slowly evolving into a competent engineer.

But if natural language prompts become the primary input mechanism for writing code, every country will have abundant local talent without needing traditional engineers. Some may dismiss this as rubbish for higher-order work and it’s true you’ll need proficiency and depth for complex tasks. But the reality is 60% of work isn’t complex.

If you do not believe me, you have not yet tried Claude Cowork yet!

Remember the 1980s? You needed specialized knowledge to operate punch cards on a mainframe to do math. Today, even basic calculators have calculus and are more powerful than yesterday’s mainframes, no engineering degree required.

AI today is where we were circa 1980s with mainframes. The Mac or Windows equivalent of AI is around the corner, coming to every pocket. Only difference, change is happening in hours not years.

If that happens, will you invest effort sourcing, hiring, developing, and running large campuses of junior developers in far-flung places with attendant risks and costs?

Or will you tap local talent like SWAT teams, move with agility, and disrupt?

Nationalism

Though advancement in communications and connectivity created real-time collaboration platforms where teams could build trust, and reverse migration of experienced talent from Western countries provided strong support, the landscape is shifting. In an increasingly nationalistic world, threats of tariffs and visa revocations create barriers that can stall or significantly increase friction. Tariffs, taxes, or bilateral barriers pose challenges for strategic programs at speed and scale. Apple exemplifies a company that has moved fast on product innovation while largely keeping talent local for these reasons. There are more examples that stay cap their global risks and will do so more in the months ahead.

Culture Shift

India’s IT talent isn’t uniform, it’s three different generations within one organizational structure.

Entry level (Gen Z and younger): They come from homes with safety nets and aren’t driven by the hustle culture of yesteryears to give their all to a job. Exceptions exist, of course. Generally, GCC talent is among the highest paid, enjoys great offices and significant benefits, and faces less work pressure compared to local startups or IT services companies. The desire to drive to the next level of performance is diminished. This is not bad but has an impact on the core premise of yesteryears.

Middle layers (Millennials): With teenage children, they’ve created financial security and seek to maintain the status quo rather than rock the boat. They want and need stability as they juggle aging parents, growing children, and higher affluence. They want to experience life.

Top management (Senior Millennials): Empty nesters with strong financial security, they want to experience life at its best. They’ve mastered managing their global leadership and are generally the most well-rounded global players.

The bottom line: the comforts and compensation of modern GCCs may have eroded the drive to constantly battle through new waves of disruption. Whether the dexterity I mentioned earlier persists or fades remains to be seen.

Risk Management

Boardrooms are realigning supply chains thanks to new tariff regimes and COVID. The same will come for CIO and CTO organizations. If I were in the boardroom, I’d ask CEOs to de-risk(hedge) by bringing core development in-country rather than waiting for a surprise change in visas, taxes, or tariffs to jeopardize the firm. The good news for India: I don’t see this as an action plan or top priority for any western organization yet. Everyone claims BCP and DR plans but the concentration risk is real. But my intuition tells me one bad actor or event will trigger this in full force and change the game.

The orthogonal risk element is the rise of sovereign LLMs.

If proprietary knowledge leaks or seeps into other copilots, it could create a huge challenge. Security implementations in GCCs are best in class, and likelihood may be low but with cloud based bots and local LLMs, we’re in uncharted waters. We don’t know who’s using which copilot on what device. LLMs can process images, so how do you manage that level of risk?

Weakening Economic Model

If the organizational structure reduces to a thin diamond shape, arbitrage erodes dramatically because higher layers of talent cost approximately 80% of their western counterparts. The compelling drive to hire abroad with all its associated risks becomes unwarranted and eats away at the need for the model itself. This is the Achilles’ heel quietly emerging beneath the surface.

Is Collapse Imminent?

No. Not yet.

Too many variables are at play for a simple answer. Environmental and ecosystem variables are uncontrollable, so we must focus on key measures.

If you are building a new GCC or just started on that journey then there are many things you can do to ensure you are future proofed. I am not covering all the recommendations for CEOs/CTOs here but a general swath of top recommendations for securing and leading the future of GCCs:

1. Model Shift

If you’re building a new GCC, build it with a radical new approach. Have a game plan for a “Force Multiplier” GCC:

For every developer you hire, ensure they’re expert in leveraging Claude or Copilot and can deliver 3x the work of current productivity benchmarks

Both speed and technical quality must be top-tier

Restrict organizational layers to 3-4 maximum from front to top, don’t scale for the sake of moving roles. Do not just shift roles. Ask will this role shift give me 3X lift.

Create a “Platoon” structure of 30-40 engineers per leader (yes, seems improbable, but it can and must be done). I have made this work so speaking from experience.

85%+ of talent must be hands-on

2. Productivity Measures

This has been controversial for ages and remains unresolved. It’s not about lack of trust but sharpening outcomes in a hyper-competitive world.

In an AI-assisted world, how do we distinguish 10 average developers from 5 rockstar developers?

There must be stringent processes and measures ensuring bloat doesn’t creep in and there are no freeloaders. I’ve encountered numerous situations where firms at HQ have no idea the amount of bloat accumulated in their GCCs, leaving money on the table with sundry and frivolous roles.

3. Accountability Roles

Over recent years, there’s been a concerted effort to bring accountability roles like CTOs or Product Heads or business heads to India, driving clear line of sight and ownership of performance at the market level. Organizations like Goldman Sachs, Adobe, and Maersk have led the way, but most GCCs pay lip service or posture more than deliver reality. Moving end-to-end accountability changes the game. I watched Nielsen Media do this with Anil Goel as CTO, he’s been a change catalyst for the firm at scale. This must be Day 1 planning, not an afterthought. Of course, it requires courage and skill at the C-suite to build a coalition without being seen as an assault on local talent and workforce.

4. India-to-India (I2I) Model

For firms where India is a large enough market, spinning off the team with autonomy for local markets can unleash exponential performance. In non-tech sectors, Unilever has done this with their India subsidiary some of their best global products were born in India. The Indian subsidiary of Unilever has been innovating for Global markets for a decade or more now. This dramatically shifts the model from cost center to value creator.

Then the scale is not about cost or arbitrage, it’s about driving market value and outcomes.

5. Government Incentives

India today has a vibrant local startup ecosystem going global with their products or taking innovations worldwide. Examples range from Whatfix, Icertis, GreyOrange to Zepto, PhonePe, Paytm and many others at significant scale. The government has been providing substantial incentives at the ground level to spawn these startups, feeding the ecosystem.

India needs a Sovereign AI Fund to invest in fast-growing AI Indian startups for the global markets.

This can meaningfully help attract, retain, and develop best-in-class products for world markets. This should be inclusive of GCC programs. Add a framework allowing independent carve-outs of GCCs to access funding support and fast-track approvals to ramp up. This progressive model can push GCCs to the next level of growth and partner with global firms to invest in innovation-centric GCCs as catalysts. Ireland has a model worth studying.

The government should also provide tax deferrals or holidays for valid AI training supported by GCCs for college graduates, enabling talent to develop high-quality AI skills rapidly making India an AI Center of Excellence for the world. This can enable GCCs to move to an entrepreneurial productization model where value accretion is much higher and eventually creates global companies at scale from India.

6. Productization

There is a lesson here from China. Once the factory of the world, it is now home to global product leaders like BYD, Huawei, Alibaba, Anker, and more. This shift transformed both talent ambition and industrial outcomes.

The same can be true for GCCs. We could have a slew of GCCs within the corporate holding structure but as separate entities or like the Unilever model, within the GCC framework, experiment, innovate, launch, and scale product platforms globally. The game is no longer dependent on older variables and paradigms. We reinvent ourselves to play a whole new product platform vision.

Firms like PhonePe, Icertis, Whatfix, and Freshworks have demonstrated that we can build the largest and best-in-class platforms in India. It just needs the right alignment of courage, skills, backing, and market opportunity. And things can take off.

Conclusion: The window to adapt is closing fast, so velocity and courage will matter

The ground will shift rapidly for GCCs in the next three years due to converging forces across the tech landscape. This isn’t a slow change but something moving at an accelerated pace. There’s an opportunity to pivot and potentially scale the GCC model to new heights but one thing is certain, it will require bold and courageous leadership that breaks many existing notions of growth.

“Picture abhi baaki hai mere dost”

Famous dialogue from an Indian film “The movie is not yet over, my friend”